- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

A Quick Guide to MSTR MicroStrategy's Bitcoin Strategy

Original Article Title: "Understanding MicroStrategy's Bitcoin Strategy in One Article"

Original Article Author: 0xCousin, IOBC Capital

In the history of Wall Street, legendary stories have never been lacking, but MicroStrategy's Bitcoin Treasury Company's strategic transformation journey is destined to become a unique new legend.

A Globally Spotlighted Bitcoin Strategy

In 2020, the COVID-19 pandemic triggered a global liquidity crisis, with countries adopting loose monetary policies to stimulate the economy, leading to currency devaluation and heightened inflation risks.

During the COVID-19 pandemic, Michael Saylor reevaluated the value of Bitcoin. He believed that with the currency's supply growing at a rate of 15% per year, people needed a hedging asset not tied to fiat cash flow. Therefore, he chose a Bitcoin strategy for MicroStrategy.

Compared to BTC ETFs launched by companies like BlackRock or other Spot Bitcoin ETPs, MicroStrategy's Bitcoin strategy is more aggressive. It purchases Bitcoin through corporate idle funds, issuing convertible bonds, share offerings, and other financing methods to gain potential gains from Bitcoin's rise while bearing potential risks from Bitcoin's fall, whereas ETFs/ETPs focus more on price tracking.

MicroStrategy's Funding Sources and Bitcoin Acquisition Journey

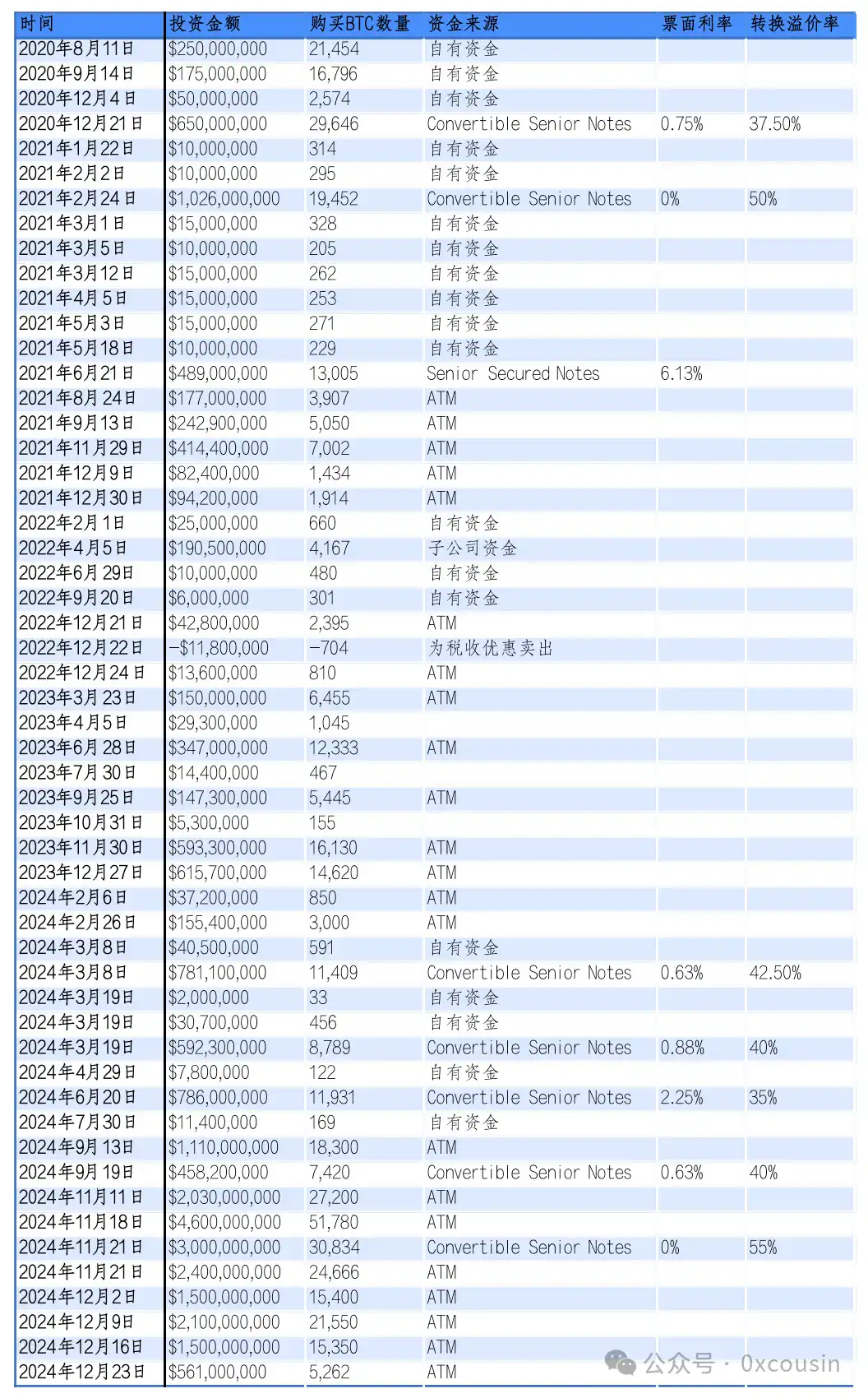

MicroStrategy mainly raised funds to purchase Bitcoin through four avenues.

1. Purchases Using Corporate Cash

For the initial three investments, MicroStrategy used its idle corporate cash for purchases. In August 2020, MicroStrategy invested $250 million to buy 21,400 Bitcoins; in September, it invested $175 million to buy 16,796 Bitcoins; in December, it invested $50 million to buy 2,574 Bitcoins.

2. Issuance of Convertible Senior Notes

To purchase more Bitcoin, MicroStrategy began using convertible bond issuance to finance its purchases.

Convertible Senior Notes are a financial instrument that allows investors to convert the bond into company stock under specific conditions. These bonds have a low or even zero-interest rate and a conversion price set higher than the current stock price. Investors are willing to purchase such bonds mainly because they provide downside protection (i.e., the bond's maturity guarantees the principal and interest) and potential gains when the stock price rises. MicroStrategy's issued convertible bonds mostly have interest rates between 0% and 0.75%, indicating that investors are confident in MSTR's stock price increase, hoping for the bonds to convert into stocks to earn more returns.

3. Senior Secured Notes

In addition to convertible senior notes, MicroStrategy has also issued $489 million of Senior Secured Notes due in 2028 with a 6.125% interest rate.

Senior Secured Notes are a type of collateralized bond with lower risk compared to convertible senior notes, but they only provide a fixed interest return. The batch of Senior Secured Notes issued by MicroStrategy has already been selected for early redemption.

4. At-the-Market Equity Offerings

As MicroStrategy's Bitcoin strategy began to show results, MSTR's stock price continued to rise. MicroStrategy opted for more At-the-Market Equity Offerings to fund its initiatives. This funding method carries lower risk as it is not debt, there is no repayment pressure, and there is no specific repayment date in sight.

MicroStrategy has entered into At-the-Market offering agreements with structures such as Jefferies, Cowen and Company LLC, and BTIG LLC. Under these agreements, MicroStrategy can periodically issue and sell its Class A common stock through these agents. This is what is commonly known in the industry as an ATM.

At-the-Market Equity Offerings provide greater flexibility, allowing MicroStrategy to choose the timing of selling new shares based on secondary market conditions. While issuing stock dilutes existing shareholder equity, the market's response to this measure has been complex due to factors such as its correlation with Bitcoin prices, the increase in MSTR's per-share Bitcoin holdings, leading to higher overall volatility in MSTR's stock price.

MicroStrategy's journey of purchasing Bitcoin through the four methods above is as follows:

Production: IOBC Capital

In the corresponding BTC price chart, MicroStrategy's specific purchase history is shown in the following image:

Source: bitcointreasuries.net

As of December 30, 2024, MicroStrategy has invested approximately $27.7 billion, acquiring 444,262 bitcoins at an average price of $62,257 per bitcoin.

Key Issues Regarding MicroStrategy's "Intelligent Leverage" Bitcoin Purchase

There has been much controversy in the market regarding MicroStrategy's "Intelligent Leverage" strategy for purchasing Bitcoin. In response to several key issues that are widely discussed in the market, I will share my thoughts:

1. How High is MSTR's Leverage Risk?

Let me start with the conclusion: it is not very high.

Based on the information disclosed by MSTR during the Q3 2024 earnings call, at that time, MSTR's total assets were approximately $8.344 billion. Because the Bitcoin carrying value in this financial report was only $6.85 billion (at that time, only 252,220 coins calculated at a price of $27,160), and the total debt was around $4.57 billion, the corresponding debt-to-equity ratio was 1.21.

We will not discuss this accounting standard, only consider the data at the time of actual sale, which reflects the latest market price. If we calculate based on the latest market price of Bitcoin on September 30, 2024 ($63,560), the actual market value of Bitcoin held by MSTR would be $16.03 billion, resulting in a MSTR debt-to-equity ratio of only 0.35.

Now, let's look at the data as of December 30, 2024.

As of December 30, 2024, MicroStrategy's total outstanding debt was $7.27385 billion, as follows:

Produced by: IOBC Capital

As of December 30, 2024, MicroStrategy held 444,262 Bitcoins, valued at $42.25 billion. Assuming that the rest of MicroStrategy's assets remain the same (i.e., $1.49 billion), then MSTR's total assets would be $43.74 billion, with liabilities of $7.27385 billion, resulting in a debt-to-equity ratio of only 0.208.

Let's take a look at the debt-to-equity ratios of some top U.S. listed companies—Alphabet 0.05, Twitter 0.7, Meta 0.1, The Goldman Sachs Group 2.5, JPMorgan Chase & Co. 1.5.

MicroStrategy is a company that has transitioned from the software industry to the financial industry, and its debt-to-equity ratio is still healthy.

2. Under what circumstances will these convertible bonds become an unbearable burden in the future?

Let's start with the conclusion: If MicroStrategy does not continue to issue convertible bonds in the future, then only if the price of Bitcoin falls below $16,364 in the long term, the value of MicroStrategy's 444,262 BTC holdings will be lower than the total amount of its convertible bonds of $7.27 billion. If MicroStrategy only uses ATM financing and idle funds to buy coins in the future without issuing more convertible bonds, as the amount of Bitcoin held by MicroStrategy increases, this "underwater" price line can become even lower.

If MicroStrategy continues to issue convertible bonds frantically to buy Bitcoin at a high price and Bitcoin enters a bear market, causing the value of MicroStrategy's Bitcoin holdings to fall below the total amount of its convertible bonds, it will also cause MSTR's stock price to slump, thereby affecting its refinancing ability and debt repayment capacity, eventually turning the convertible bonds into an unbearable burden.

Holders of MicroStrategy's convertible bonds have the right to convert their bonds into MSTR's stock, which is divided into 2 stages: 1. Initial stage - If the bond's trading price drops by>2%, the bondholder can exercise the conversion option, convert the bond into MSTR shares, and sell to recoup the principal; if the bond's trading price remains normal or even rises, the bondholder can sell the bond in the secondary market at any time to recoup the principal. 2. Later stage - When the bond is about to mature, the 2% rule no longer applies, and the bondholder can either take the cash and leave or directly convert the bond into MSTR shares.

Since MicroStrategy's issued convertible bonds are all low-interest or even zero-interest bonds, it is clear that bondholders are actually looking for a conversion premium. If, on the repayment date, the MSTR stock price has increased compared to the price at the time of financing, then the bondholders are more likely to consider converting the bonds into shares. If the MSTR stock price has decreased compared to the price at the time of financing, then the bondholders will consider receiving the principal and interest.

If bondholders do not choose to convert into MSTR shares and actually need repayment, MicroStrategy also has several options:

· Continue to issue new shares to raise funds for repayment;

· Continue to issue new bonds to repay the old ones; (This was done in September 2024)

· Sell some of the Bitcoin to use for repayment.

Therefore, at present, the likelihood of MicroStrategy falling into an "underwater" situation is not high.

3. Why are investors starting to care about MSTR's per-share coin holdings?

Let's start with the conclusion: Per-share coin holdings will determine MSTR's per-share net asset value.

Whether through issuing convertible bonds or ATM offerings, financing is achieved through share dilution. The purpose of this financing is to increase the Bitcoin reserve. For MSTR shareholders, share dilution is a negative signal, traditionally speaking, not a favorable development. The story MicroStrategy's management tells its shareholders is the BTC Yield KPI.

In essence, as long as MSTR's market capitalization is higher than the total value of the held BTC, creating a market value premium, diluting MSTR's shares to buy BTC can increase MSTR's per-share coin holdings. An increase in MSTR's per-share coin holdings means an increase in MSTR's per-share net assets. Therefore, for shareholders, diluting shares to finance the purchase of Bitcoin is still a worthwhile endeavor.

Currently, MicroStrategy holds 444,262 BTC, with a total holding value of approximately $42.256 billion. With MSTR's current market capitalization at $80.37 billion, MSTR's market cap is 1.902 times the Bitcoin holding value, resulting in a current premium of 90.2%. Currently, MSTR has a total share count of 24 million, with each share corresponding to approximately 0.0018 BTC.

This is the essence of "intelligent leverage," converting the difference between its corporate market value and Bitcoin holding market value into a capital operation advantage.

4. Why has MicroStrategy been more aggressive in buying Bitcoin in the past two months?

Let's start with the conclusion: It may be because MSTR's stock price is very high.

In the past two months, MicroStrategy has significantly increased the scale of its coin acquisition through financing. In November and December 2024, MicroStrategy invested a total of $17.69 billion (representing 63.8% of the total investment amount) in purchasing 192,042 bitcoins (representing 43.2% of the total purchase amount) through ATMs and convertible bond offerings. Only $3 billion was from convertible bonds, while the remaining $14.69 billion was financed through ATMs.

Overall, MicroStrategy's strategic allocation of Bitcoin appears to have characteristics of dollar-cost averaging over time. However, in terms of quantity and amount, it seems to be more aggressive in buying during a bull market than in a bear market.

I couldn't understand this feature and could only make a bold guess. It might be because during the bull market, MSTR's stock price saw a higher increase. In August 2024, after a stock split, MSTR's stock price tripled, with a more than fourfold increase throughout the year, while Bitcoin only saw a 2.2-fold increase this year.

MicroStrategy's CEO discussed a beautiful "42B Plan" during the Q3 2024 earnings call.

British author Douglas Adams said in "The Hitchhiker's Guide to the Galaxy" that the supercomputer Deep Thought provided the answer "42" as the ultimate answer to "Life, the Universe, and Everything."

MicroStrategy considers this a magical number and has thus proposed the 42B financing plan. 21 is also a magical number as Bitcoin's maximum total supply is 21M. Therefore, MicroStrategy plans to issue 21B ATM + 21B Fixed Income in the next three years to continue accumulating Bitcoin.

If MicroStrategy eventually raises $42 billion through share issuance, assuming an issuance at a $330 share price, the total share capital post-issuance would become 371.3 million shares. Assuming MicroStrategy buys Bitcoin at an average price of 100,000 USD, the company could acquire 420,000 bitcoins, bringing MicroStrategy's total holdings to 864,262 bitcoins. At that point, the bitcoin holdings per share would increase to 0.00233, a growth of about 29.4%. At this time, MSTR's total market capitalization would be $1,225.3 billion, with the total value of BTC holdings at $864 billion. In this scenario, a market value premium would still exist.

5. What Will Drive Bitcoin's Price Up After MicroStrategy?

Starting with a conclusion, besides publicly traded companies buying Bitcoin driven by MicroStrategy, the only other significant potential driver is more national-level strategic reserves, but expectations shouldn't be too high in this bull market cycle.

During this cycle, some of the major Bitcoin buyers are:

1. Long-Term Holders with Strong Consensus on Bitcoin

Bitcoin's long-term uptrend doesn't need a reason; in the eyes of BTCers, it's as natural as monkeys climbing trees or mice digging holes because it is digital gold.

After Bitcoin fell below $16,000, at that time, the most mainstream Antminer S17 series miners were shut down near the shutdown price, and miners like the Whatsminer M30S, Whatsminer M30S, and Antminer T19 had already reached the shutdown coin price range. In this price range, even if nothing happens, a bounce will occur. The bull-bear transition is like a basketball falling freely from a height, bouncing sequentially weaker after hitting the ground.

Source: glassnode

As can be seen from the above chart, by the end of 2022, Long Term Holders continue to accumulate.

After more than a decade of development, the Bitcoin consensus has become strong enough, with on-chain hodlers and Long Term Holders reaching a consensus near the mainstream miner shutdown price.

2. ETF Bringing Incremental Capital from Traditional Financial Markets

Since the introduction of BTC ETFs, a total of 528.6k BTC have been net inflowed. In this bull market cycle, ETFs have brought nearly 36 billion in incremental buying pressure to Bitcoin, and 2.6 billion to ETH.

Source: coinglass.com

Furthermore, the approval of BTC ETFs (and ETH ETFs) will also have a driving effect, with more traditional financial institutions starting to pay attention to and enter the Crypto space.

3. MicroStrategy Continues to Buy, Multiple Public Companies Follow Suit, Davis Double Click

According to Bitcointreasuries data, as of December 30, 2024, 149 entities collectively hold over 2.95 million BTC. This data is still growing rapidly in recent times.

Source: bitcointreasuries.net

Among these entities holding Bitcoin, there are 73 public companies, 18 private companies, 11 countries, 42 ETFs or Funds, and 5 DeFi protocols.

MicroStrategy was the first public company to adopt a "Bitcoin Treasury Company" strategy, but not the only one. Other public companies such as Marathon Digital Holdings, Riot Blockchain, Boyaa Interactive International Limited, among others, have also implemented this strategy. However, MicroStrategy still has the largest impact.

4. National Strategic Reserves

Currently, some governments hold Bitcoin. Specific details are as follows:

Source: bitcointreasuries.net

Although these countries hold Bitcoin, most of the Bitcoin was seized by law enforcement agencies during law enforcement processes. It is temporarily not being sold and does not belong to a stable Holder.

Among these countries, perhaps only El Salvador is a true BTC Holder. Since 2021, El Salvador has been buying Bitcoin, purchasing 1 BTC per day. As of now, they hold 6,002 BTC, valued at over $560 million.

Furthermore, Bhutan holds 11,688 BTC through Bitcoin mining. However, Bhutan is not considered a BTC Holder and has recently reduced its holdings in the past two months.

During his election campaign, former U.S. President Trump once stated that if he were elected president, he would establish a strategic Bitcoin reserve.

If MicroStrategy paved the way, one could argue that there is no greater force to drive Bitcoin's rise than Trump taking office and pushing for a U.S. government Bitcoin strategic reserve, subsequently leading to more countries strategically reserving Bitcoin.

Conclusion

MicroStrategy's Bitcoin strategy is not just a corporate transformational business experiment but also a significant innovation in financial history. Through clever capital operations, intelligent leverage, and a profound insight into Bitcoin's value, it has not only achieved brilliant market value growth for itself but has also more profoundly brought Bitcoin into the traditional financial landscape, breaking down the barriers between crypto assets and mainstream capital markets.

MicroStrategy's bold attempt may only be the prelude to Bitcoin's legend or perhaps an insignificant step in Bitcoin's true rise, but it could be a significant step toward a new financial era.

References:

https://www.microstrategy.com/press/microstrategy-announces-third-quarter-2024-financial-results-and-announces-42-billion-capital-plan_10-30-2024

https://www.hope.com/for-corporations

https://bitcointreasuries.net/

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.