Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

AI has simultaneously created a shortage and surplus of memory

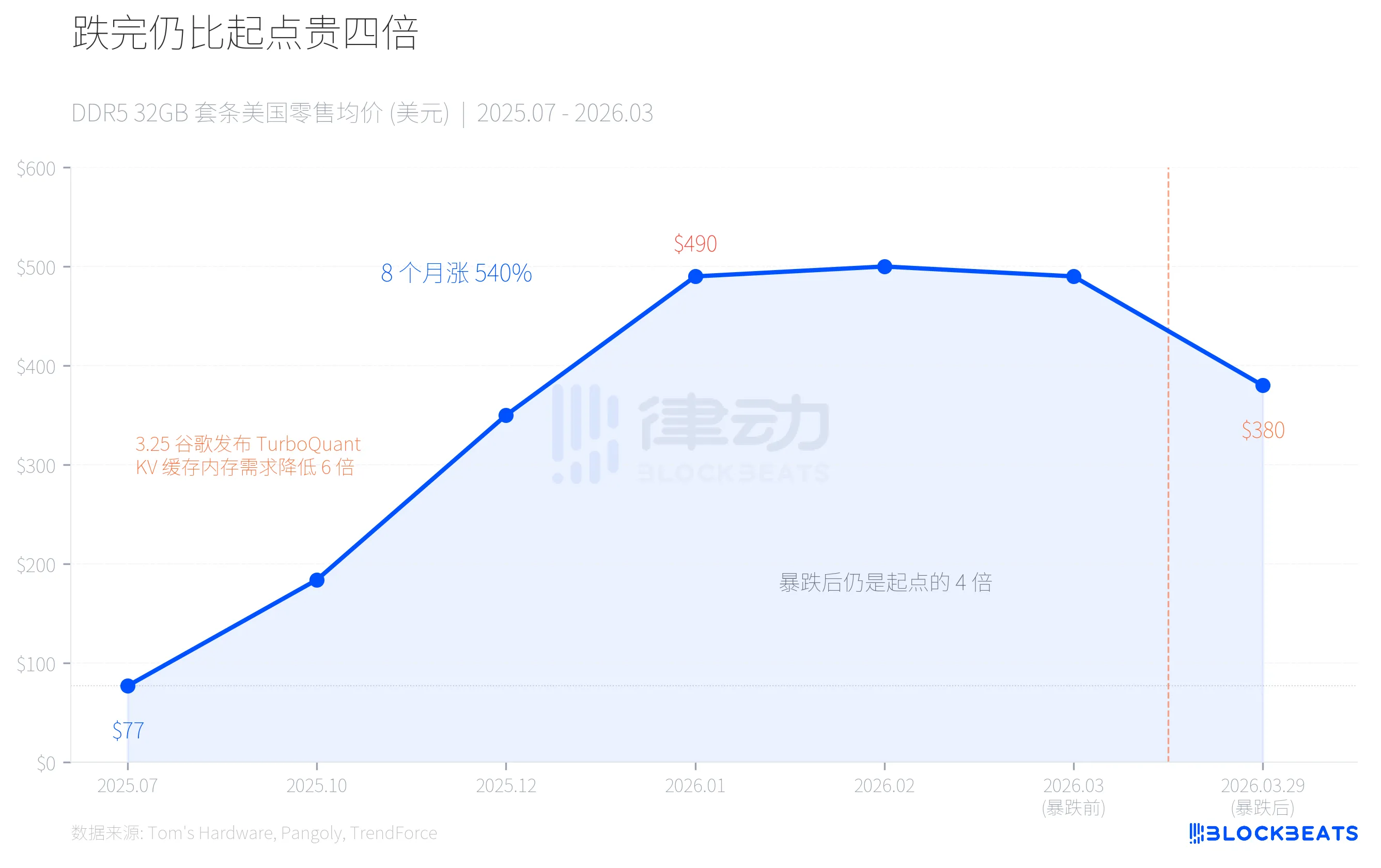

On March 29, both Huaqiangbei and the U.S. retail market simultaneously experienced a cliff-like drop in memory prices. The Corsair 32GB DDR5-6400 kit plummeted from $490 to $380, a single-day drop of 22%. Domestically, the price of a 32GB DDR5 high-speed kit fell by 800 yuan in a week, leading to panic selling among channel distributors, with some stating "it dropped more than 100 bucks in a day."

However, when this number is placed on a longer timeline, the picture is completely different: even after the drop, the current DDR5 price is still four times that of July 2025. It was a precise supply-demand mismatch in the AI industry chain, where the same force first created a shortage and then generated surplus panic.

Roller Coaster: 540% Increase in Eight Months, 22% Drop in One Month

In July 2025, a mainstream 32GB DDR5-6000 kit in the U.S. retail market was only $77. By January 2026, the price of the same kit surged to $490. A 540% increase in eight months.

The price increase was not due to consumers suddenly crazy about upgrading their computers. According to TrendForce data, in the first quarter of 2026, DRAM contract prices rose by 90%-95% on a quarter-on-quarter basis, with PC DRAM prices increasing by over 100%, marking the largest quarterly increase on record. Driving all this was the AI infrastructure's thirsty demand for a particular type of memory.

Then, on March 25, Google released a compression algorithm called TurboQuant. Four days later, memory prices collapsed.

Where Did the Capacity Go? HBM Ate Your Memory Stick

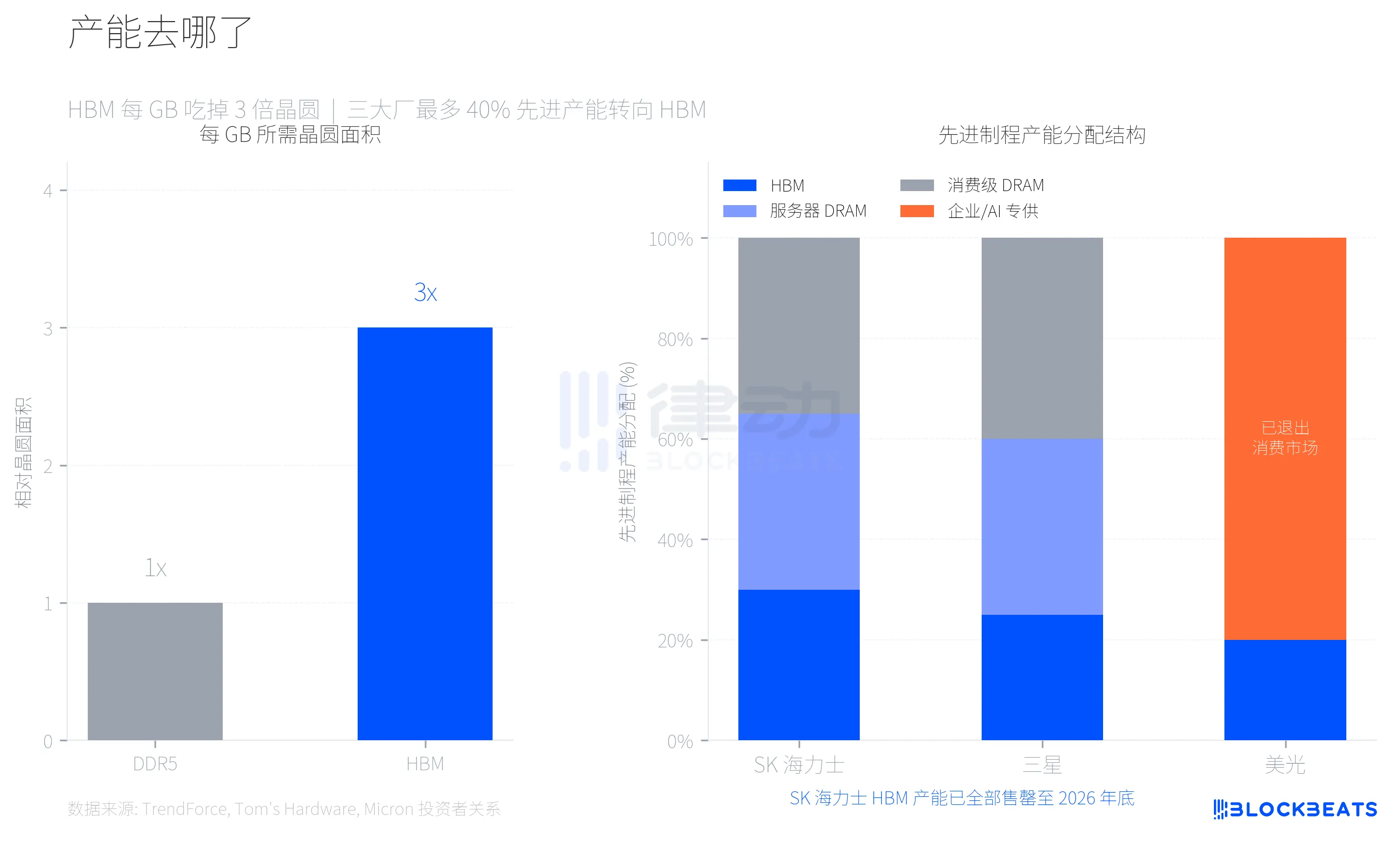

To understand this price surge, you first need to grasp a key technical parameter. HBM (High Bandwidth Memory, dedicated memory for NVIDIA AI chips) consumes three times the wafer area per GB compared to regular DDR5. According to Tom's Hardware, this means that, from the same wafer, producing HBM only yields one-third the capacity of DDR5.

Samsung, SK Hynix, and Micron, the three major memory manufacturers, made a rational choice in the face of the high-profit margins of HBM, shifting up to 40% of their advanced process wafer capacity to HBM production. According to TrendForce data, in the first quarter of 2026, DDR5's profit margin is expected to exceed that of HBM3e for the first time, indicating to what extent the supply of consumer-grade memory has been squeezed.

Micron's choice is the most radical. In December 2025, the company announced the closure of its 29-year-old consumer brand Crucial, completely exiting the consumer-level memory and storage market, and fully turning to enterprise and AI customers. According to Micron's Investor Relations announcement, its total revenue for the 2025 fiscal year was $37.38 billion, with data center and AI applications accounting for 56% of total revenue. The consumer market is not worth pursuing.

SK Hynix's HBM capacity has been completely sold out until the end of 2026. Samsung plans to increase its HBM monthly capacity from 170,000 wafers to 250,000 wafers by the end of 2026. The new wafer fabs (Samsung P4L and SK Hynix M15X) are not expected to start mass production until 2027-2028 at the earliest. In other words, the supply gap for consumer DRAM is structural and cannot be alleviated in just one or two quarters.

Transformation of the Landscape: SK Hynix Breaks Samsung's 40-Year Dominance

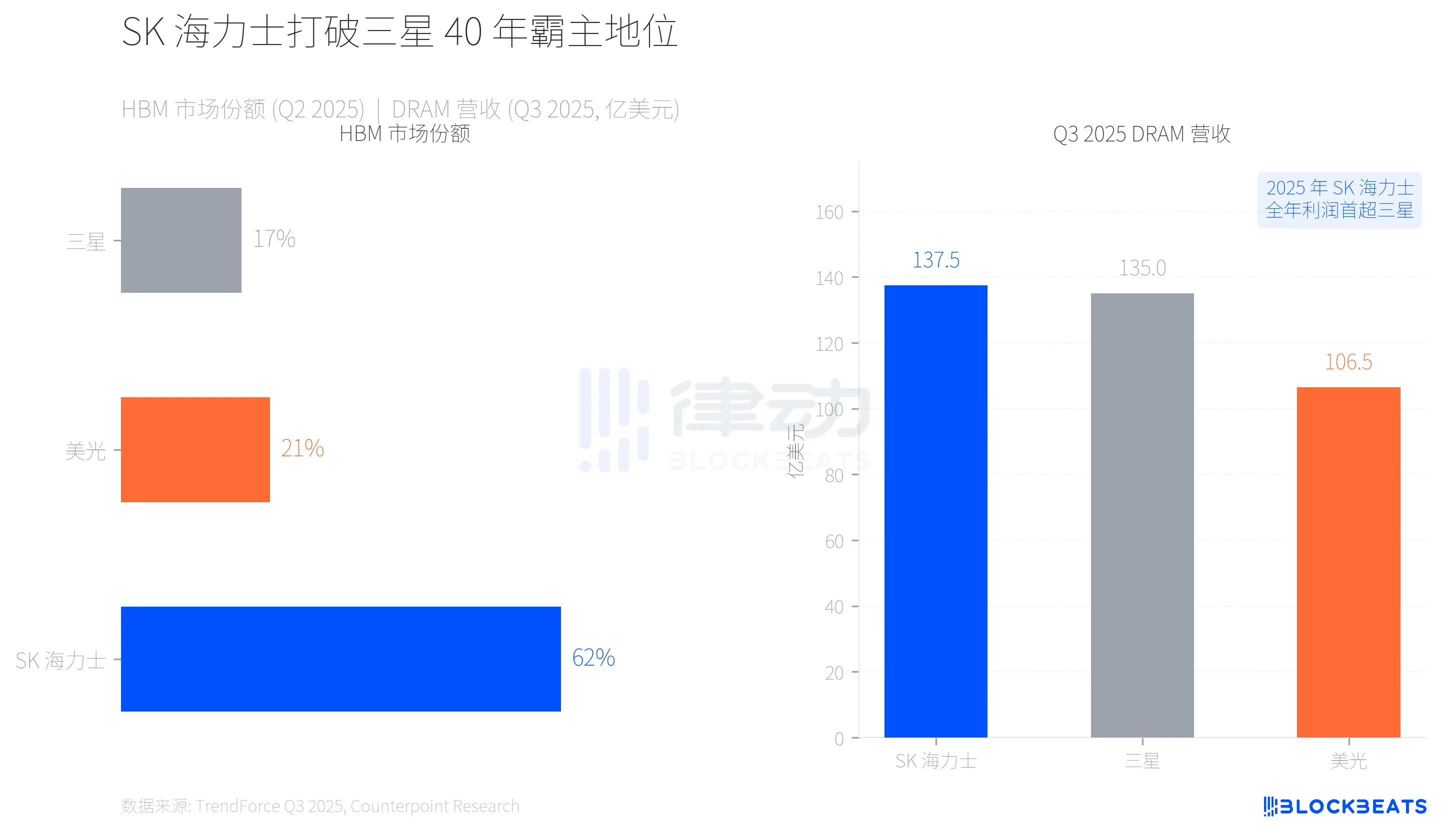

This capacity shift has also reshaped the power structure of the memory industry. According to TrendForce data, in the second quarter of 2025, SK Hynix, with deep ties to NVIDIA, captured 62% of the HBM market, while Samsung held only 17% and Micron 21%.

Even more significantly, there has been a revenue-level turnaround. According to TrendForce's Q3 2025 report, SK Hynix topped the single-quarter DRAM revenue for the first time with $13.75 billion, followed closely by Samsung at $13.50 billion. The gap between the two was only $250 million, but this marks the first time in nearly 40 years that Samsung has lost its top position in memory revenue. CNBC reported that SK Hynix's full-year operating profit in 2025 also surpassed Samsung's for the first time.

The HBM first-mover advantage has given SK Hynix enough leverage, but this race is far from over. Samsung is working hard to catch up in the mass production progress of HBM4, and while Micron has abandoned the consumer market, its revenue growth in the enterprise and AI fields (Q3 QoQ +53.2%) is the fastest among the big three.

How Did an Algorithm Rock the Logic of Price Increases?

On March 25, Google presented the TurboQuant algorithm at ICLR 2026. This algorithm did one thing: it compressed the KV cache (Key-Value cache, the most memory-intensive part during language model inference) from FP16 precision to 3-bit, reducing memory usage by at least 6 times, while achieving up to 8 times attention computation acceleration on the H100 GPU. According to the Google Research Blog, in five long-context benchmarks like Needle-in-a-Haystack, precision loss was zero.

The market quickly did the math. If TurboQuant or a similar algorithm is widely adopted by mainstream AI companies, then AI inference's incremental demand for DRAM will significantly shrink. The core narrative that has supported the rise in memory prices over the past year and a half is precisely that "AI infrastructure has consumed too much memory capacity."

Four days later, channel confidence collapsed.

It should be noted that TurboQuant targets KV caching on the AI inference side, not HBM demand on the training side. The supply-demand relationship for HBM will not change in the short term due to an inference optimization algorithm. However, the market does not always distinguish between the two. According to Sina Finance, before the crash, a large number of off-channel hoarders rushed into the domestic channel due to price increases, with high prices causing a retail sales plunge of over 60%. Chain selling under a tight funding chain magnified the decline.

An AI industry chain has simultaneously created a shortage and surplus panic for memory. The physical capacity squeeze of HBM has made consumer-grade memory in short supply, while TurboQuant's algorithmic efficiency breakthrough has caused a sharp drop in AI memory demand expectations. The same force is behind both the price hike and the market collapse.

You may also like

OpenClaw 3.28 Update: Potential Security Risks with Axios

Key Takeaways Recent findings suggest OpenClaw version 3.28 may contain a compromised version of the Axios library. Dependency…

Steakhouse Financial Experiences Phishing Attack: A Comprehensive Overview

Key Takeaways Steakhouse Financial’s domain experienced a phishing attack, prompting user safety advisories. Depositors’ funds and smart contracts…

DeFi Risk Management in Turmoil: Gauntlet’s Bold Move Amidst Resolv Exploit

Key Takeaways Gauntlet, a leading DeFi risk manager, is engaging in full recovery efforts after Resolv Labs’ exploit.…

FTX/Alameda Wallet Transfers Over $8 Million in ZRO Tokens to Wintermute

Key Takeaways An FTX/Alameda-associated wallet moved 4.126 million ZRO tokens to market maker Wintermute, with an approximate value…

Analysis of Recent Ethereum Short Position Activity on HyperLiquid

Key Takeaways Recently, a newly created wallet deposited $4.89 million into HyperLiquid, opening a short ETH position with…

Only 43% ROI on $1, why are 87% of Polymarket traders in the red?

After L2 Fraud, Ethereum Turns to ‘Economic Zone’ Self-Help

How Can the Average Person Win in the 2026 AI Boom?

When Wall Street Meets Crypto, Here's Your "Stock Market Beginner & Advanced Guide"

StandX Introduces SIP1 and SIP2: Holding Subsidy Mechanism Launched, Reshaping On-Chain Trading and Reward Structure

Decoding Aave V4: A Shift from Product to "Banking"

Huobi HTX Releases "2026 Digital Asset Trends Whitepaper": Global Liquidity Reconfiguration, Defining the New Era of "On-Chain Finance"

PUMP Valuation Breakdown: Debunking On-Chain Data “Wash Trading” Narrative, Where Does the Real Discount Come From?

StandX launches SIP1 and SIP2: Position subsidy mechanism goes live, reshaping on-chain trading and revenue structure

Huobi HTX Releases the "2026 Digital Asset Trend White Paper": Global Liquidity Restructuring, Defining a New Sovereign Era of "On-Chain Finance"

DeFi Governance Revolution

Encrypted CEX is becoming a historical species

Who Pays for War? | Rewire News Morning Digest

OpenClaw 3.28 Update: Potential Security Risks with Axios

Key Takeaways Recent findings suggest OpenClaw version 3.28 may contain a compromised version of the Axios library. Dependency…

Steakhouse Financial Experiences Phishing Attack: A Comprehensive Overview

Key Takeaways Steakhouse Financial’s domain experienced a phishing attack, prompting user safety advisories. Depositors’ funds and smart contracts…

DeFi Risk Management in Turmoil: Gauntlet’s Bold Move Amidst Resolv Exploit

Key Takeaways Gauntlet, a leading DeFi risk manager, is engaging in full recovery efforts after Resolv Labs’ exploit.…

FTX/Alameda Wallet Transfers Over $8 Million in ZRO Tokens to Wintermute

Key Takeaways An FTX/Alameda-associated wallet moved 4.126 million ZRO tokens to market maker Wintermute, with an approximate value…

Analysis of Recent Ethereum Short Position Activity on HyperLiquid

Key Takeaways Recently, a newly created wallet deposited $4.89 million into HyperLiquid, opening a short ETH position with…