Founder's BIO New Article: From Science Fiction to Science Finance, How Does Desci Drive the Biotech Revolution?

Original Article Title: From Science Friction to Science Finance: A Community-Driven Revolution in Biotech

Original Article Author: Paul Kohlhaas, Founder of BIO Protocol

Original Article Translation: zhouzhou, BlockBeats

Editor's Note: This article introduces how the BIO Protocol addresses funding, R&D, and market issues in the biotechnology field through the decentralized BioDAO network. By tokenizing intellectual property, implementing decentralized governance, and providing real-time liquidity, BIO enables patients, scientists, and investors to participate in decision-making together, supporting neglected areas such as rare diseases and long-haul COVID. BIO breaks through traditional fund structures, drives innovation in biotechnology, accelerates the research process, achieves more efficient and equitable capital flow and results transformation, ultimately promoting scientific advancement and global impact.

The following is the original content (reorganized for better readability):

“We live in a society exquisitely dependent on science and technology, in which hardly anyone knows anything about science and technology.” — Carl Sagan

TL;DR

· The Broken Biopharma System: Science Hits a Bottleneck

· Andrew Lo's Mega Fund Theory: A Milestone in Biotech Finance

· Beyond Mega Funds: Emergence of the BIO Protocol

· From Fund to Ecosystem: Advancing Lo's Vision in the BioDAO Network

· Practice of the BIO Protocol

· Orphan Drugs, Rare Diseases, and Long-Haul COVID: Ethical and Economic Alignment

· Lessons from Mega Fund-Inspired Biotech Holding Companies

· From Science Friction to Science Finance

· Bottom-Up Financial Evolution

A universal truth shrouds our modern era where scientific knowledge is exploding, yet life-changing therapies — from long-haul COVID to rare autoimmune diseases — remain elusive for millions. This stark contrast reveals a distorted paradox: the issue is not scientific impossibility but rather inefficiencies in market structure.

Big Pharma pours billions into incrementally improving existing drugs (like enhancing existing PD-1 cancer drugs or GLP-1 anti-obesity drugs) through strategies such as patent lifecycle management, chasing after the latest and hottest clinically validated drug targets in a fiercely competitive market — while research into patient-driven needs languishes.

What is the result? An industry mired in scientific friction, with escalating costs, capital bottlenecks, and intellectual property islands that slow down potential transformative innovations, even leading to their complete abandonment.

1. Fragmented Biopharma System, Science Hitting a Roadblock

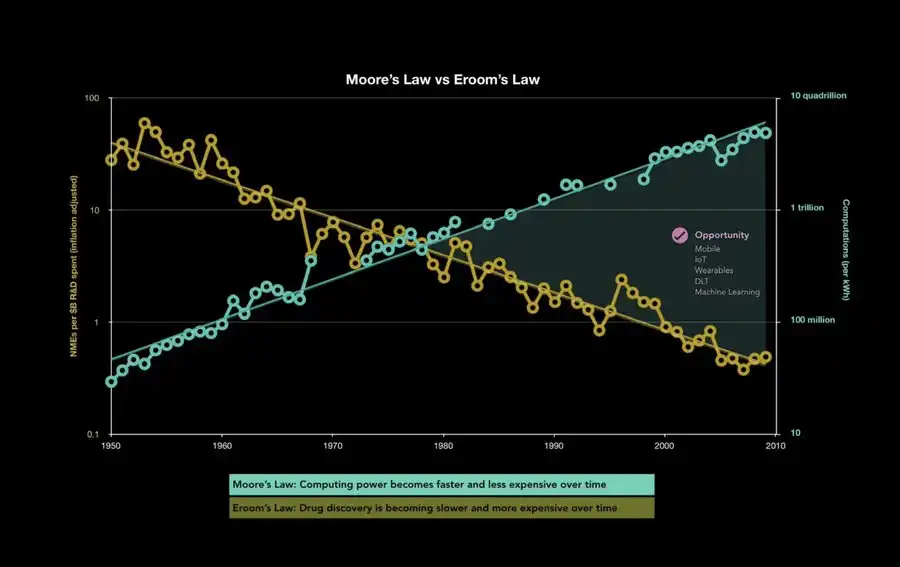

Every day, millions of people are battling long-term, complex, fragile, and underfunded diseases like COVID-19. Many find that the research to help them is not "hard" in a scientific sense but rather "hard" in terms of the return on investment (ROI) for traditional pharma. This is just a symbol of a broader crisis, as revealed by Eroom's Law: as biotech R&D spending has soared, the productivity of discovering new drugs has plummeted. How did we get here?

1.1 Valley of Death and the "Safe Bet"

Promising discoveries made in academia often struggle to transition to early clinical research because no one is willing to fund the risky transition stage between animal studies and human trials. This infamous "Valley of Death" hinders potential treatments that, in the eyes of major pharmaceutical companies, lack profit potential and are too high-risk.

Many venture capitalists and pharma companies take a "fast follower" approach, waiting and hoping that other companies will successfully navigate these risks. These risks may include understanding the pathophysiology of a disease, addressing regulatory challenges (such as a lack of clear clinical endpoints), the uncertain commercial viability of a pharma M&A, or the dynamics of health insurers in reimbursing treatments. It is a minefield of incentives and constraints with no collective mechanism empowering the patient voice.

1.2 Overconcentration of Capital

The primary funding channels for biotech—large pharma companies and major venture capital firms—often concentrate investment in "blockbuster" categories. Over 90% of biotech capital is concentrated in highly competitive, minimally differentiated areas, causing once-promising breakthrough research (such as longevity, complex immune system diseases, or neuroscience) to stagnate.

While these clinically lower-risk and commercially appealing therapy areas are attractive to pharma companies and venture capitalists, many areas also represent the most expensive failures, as only 5% of approved and marketed drugs achieve blockbuster sales potential.

Otherwise, it is a waste of substantial R&D funding. In Bruce Booth's renowned "Atlas 2024 Review," Bruce commented that less than 15% of biotech financing rounds have captured over 66% of available venture capital funding, a significant shift from the situation ten years ago. We need more meritocratic mechanisms to address public health challenges and the impending Western societal demographic tsunami.

1.3 Intellectual Property Lock-In and Data Silos

Under the current business model, knowledge is trapped behind thick walls of patents and closed-door deals, slowing down progress. Global labs often repeat the same high-cost experiments due to a lack of shared insights, adding unnecessary friction. Patient data and clinical insights are so fragmented that under a unified data architecture, they could hold significant inferential value, but are plagued by bureaucratic hurdles from institutions like hospital administrators, data aggregators, and biobanks.

Intellectual property may be time-bound and only certain forms (like composition of matter patents) hold significant value for venture capitalists and pharmaceutical companies, which goes against the longevity community's enthusiasm for repurposing drugs such as rapamycin, metformin, and spermidine. Overall, inefficient resource allocation and commercial constraints hinder real-world health transformation, where real-time transparency can help alleviate some of these issues.

1.4 Opaque R&D and Limited Accountability

The R&D pipeline's unfolding process is slow and convoluted. Flow of funds is opaque; external parties cannot see whether (or why) trials have failed until it's too late. There is limited accountability, leaving patients and the public in the dark.

Executive management and R&D teams are in constant flux, with the pipeline changing along with the team. Companies like Roivant have built successful large enterprises by strategically shelving drugs through licensing and development agreements.

1.5 Over 10-Year Funding Lock-In Suppresses Innovation

Traditional biotech investments often require a decade or more to see returns—which is almost an eternity in the fast-paced market. This illiquidity leads to early-stage research lacking funding, especially in cases of uncertain outcomes.

Biotech competes for capital allocation against other asset classes such as more easily understandable revenue/EBITDA growth. In this scenario, an open community helps bridge the relative value gap of these therapies in terms of education and socialization.

Biotech is at a disadvantage in attracting investors and gaining market share, while other health-related themes (such as longevity) have become cultural phenomena. Some biomedical breakthroughs (like statins, PD-1 inhibitors, or anti-obesity drugs) demonstrate remarkable commercial potential (e.g., the 2024 Obesity 5 (NONO, LLY, AMGN, ZEAL, and VKTX) yielded a 93% return), but the investment structure needs significant revision to ensure the value of these transformative innovations is not diluted and to ensure better investor access—this is where tokenization will bring about transformative change.

Eroom's Law is at odds with the tremendous scientific advances we are currently experiencing — such as DeepMind's AlphaFold2, the 2024 Nobel Prize in Chemistry, mRNA therapy, GLP-1, cell and gene therapy, and more. The commercial and vested interest models of the pharmaceutical and biotech industries have hardly been questioned, and if there are operational structures that can help improve efficiency, they will be warmly welcomed.

Andrew Lo's Mega-Fund Theory: A Milestone in Biotech Finance

In 2012, Professor Andrew Lo from MIT and his collaborators proposed the concept of a "mega-fund" — a large, diversified early-stage drug candidate pool. Having 50 to 200 relatively unrelated assets can spread risk: while a single biotech startup may fail if its sole treatment approach falters, a portfolio can withstand multiple failures as long as a few successful projects can bring returns.

This theory groundbreaking pointed out the structural inefficiency in funding life science research. However, Lo's approach is still top-down: large checks from institutional investors, top-down fund allocation, with little opportunity for ordinary scientists or patients to participate in meaningful decisions.

3. Moving Beyond the Mega-Fund: Introducing the BIO Protocol

Now, a new wave of decentralized science has emerged, furthering Lo's vision. The BIO Protocol has drawn on the core concept of the mega-fund — managing risk through broad diversification — but reimagined the way this diversification, governance, and capital formation occur. The BIO Protocol is not like a centrally managed single massive fund but:

· Serves as a decentralized token-holder-governed protocol planning and incubating BioDAO. These are dedicated bottom-up communities guiding research through on-chain research portfolios.

· Tokenizes intellectual property and data through IPT (Intellectual Property Tokens) to make them tradable liquid assets, enabling BioDAO researchers and communities earlier access to liquidity than the conventional biotech industry setup.

· Deploys capital in real-time, directly into the "valley of death."

· Places patients, scientists, and laypeople at the center, akin to Reddit communities having a shared bank account.

3.1 Permissionless Stakeholders

In BioDAO, anyone directly linked to a particular disease — be it patients, clinicians, or scientists — can join through on-chain governance. Instead of passively hoping for "someone" to fund their endeavors, they collectively crowdfund capital through encrypted funds, form a DAO, collectively source research ideas from internal and global scientists, and decide on resource allocation and priority development.

3.2 Tokenized Intellectual Property and Data

BioDAO has released IP Tokens (IPT) through @molecule_dao, representing decentralized governance rights over research. These tokens can be licensed, traded, or pooled, effectively providing a new way for DAOs to gradually de-risk early-stage science based on milestone-based fund deployment. Shared data and data replication are no longer an afterthought but a core, liquid asset that can drive scientific discovery. Bonuses can also be issued to various researchers, creating incentives for decentralized science and drug discovery.

3.3 Bottom-Up Capital Formation

Unlike giant funds relying on large institutional investors, the BIO protocol coordinates community-driven fundraising. Through its launchpad, BioDAO founders can showcase their research, set up private or public token sales, and reward early supporters with governance rights—without the need for VC or Big Pharma scrutiny.

4. From Fund to Ecosystem: Advancing Luke's Vision in the BioDAO Network

4.1 Decentralized Center of the "Meta Portfolio"

The BIO protocol does not hold 200 assets like a single entity but facilitates a governance treasury with thousands of BioDAOs, each focusing on a scientific subfield. This significantly expands the space of possibilities while enabling community self-governance. There is no single manager making decisions; instead, the protocol guides asset development, risk management, and synergies for all these DAOs through its token holder community.

4.2 Permissionless Launchpad and Acceleration

BIO’s real-time decentralized launchpad mechanisms—such as bonding curves or auctions—enable new BioDAOs to launch quickly. Early stakers or token holders can signal which areas are worth investing in. This approach democratizes biotech funding and accelerates capital flow to overlooked areas like long COVID or rare autoimmune diseases.

4.3 On-Chain Risk Management

Just as giant funds use portfolio theory to reduce risk, BioDAO does the same, but on-chain analytics enable them to share standardized reports on clinical milestones, intellectual property valuations, and treasury data. This facilitates real-time insights, allowing the protocol to diversify risk across multiple DAOs or rebalance further through research-based obligations.

4.4 Continuous Liquidity and Evergreen Capital

Traditional funds lock capital for ten years, while BioDAO's tokens and intellectual property tokens maintain liquidity, allowing participants to exit or reallocate capital. If a BioDAO's therapy begins to show promise, it naturally attracts more liquidity. The game theory here is that the treatment will naturally become a capital "Schelling point." Meanwhile, revenue from successful therapies flows back to the protocol treasury (BIObank), recycling capital into new or existing DAOs.

5. Protocol in Action: A Holistic, Bottom-Up Ecosystem

Imagine a team of scientists proposing a new "NeuroDAO" aimed at developing innovative therapies for traumatic brain injury. They upload preclinical data and a funding roadmap to BIO's user-friendly launchpad. The global BIO community approves or rejects the proposal through token staking—no closed-door operations by a small committee behind the scenes. Upon approval:

· NeuroDAO mints its intellectual property tokens (IPTs).

· These tokens are sold through bonding curves or auctions to raise initial capital.

· As milestones (e.g., preclinical endpoints) are met, more capital automatically unlocks.

· The broader community can track progress, further invest, and accelerate the flywheel effect.

If NeuroDAO reaches a significant breakthrough moment—like discovering a new molecule that accelerates brain recovery—the intellectual property licensing agreement can channel revenue back into the treasury to fund further research. This mechanism creates a sustainable flywheel effect, driving an evergreen, self-reinforcing cycle.

Since its inception, the BIO ecosystem has experienced rapid growth. In less than two years:

· 8 BioDAOs have been funded

· $30 million has been raised for research

· Total value of tokenized intellectual property exceeds $50 million

· Funds in the BIO treasury (AUM) exceed $60 million

· $8 million has been allocated to scientific projects funded by BioDAOs to date

· 60 active research projects

· 34,000 ecosystem token holders (3,716 of whom hold BIO governance tokens)

Several BioDAOs have rapidly progressed from the seed stage of research to advanced preclinical research, validating that decentralized capital plus open collaboration can accelerate biotechnology innovation.

Orphan Drugs, Rare Diseases, and Long COVID: The Ethical and Economic Intersection

Long COVID is just one example of a "niche" yet urgent condition. Similarly, orphan diseases—those affecting smaller patient populations—are often overlooked by major pharmaceutical companies because they see limited profit potential.

However, within networks like BIO, patient-led or family-led BioDAOs can be established around any disease, using novel structures to fund research that large companies are unwilling to sponsor. Smaller patient populations can accelerate clinical trials, shorten timelines, and unlock substantial returns without the "blockbuster or bust" mindset. The ethical alignment is clear: this is not about market size but about impact.

7. Real-World Momentum: Insights from Company Models Inspired by Mega Funds

Prior to decentralized science, the multi-asset risk-sharing model has been attempted in various forms:

· BridgeBio (NASDAQ: BBIO): Focused on rare diseases, employing a hub-and-spoke pipeline.

· Roivant Sciences: Introducing separate "Vants" for each therapeutic area, integrating management fees and capital.

· Royalty Pharma: A portfolio with billions in diversified royalty income streams, demonstrating securitization can stably fund drug IP.

These companies reflect Lo's principle of diversification. The BIO protocol further extends this principle through democratizing access, distributing governance, and achieving ongoing liquidity through tokenization.

8. From Scientific Fricton to Science Finance (SciFi)

Close your eyes and imagine it's now 2026. Within the BIO framework, there are already hundreds of BioDAOs spanning various diseases from pancreatic cancer to autoimmune alopecia. Each DAO is a "community collective intelligence" composed of patients, researchers, and philanthropic supporters. They:

· Access real-time research data shared across networks, accelerating progress at each clinical inflection point.

· Coordinate clinical trial participants and best practices (if multiple BioDAOs are addressing related domains, BIO can facilitate shared trial participant pools, data registries, and best practices governance, reducing management overhead).

·Using AI to assess risk, potential synergy, and capital allocation.

No longer are decade-long capital lockups or fortress-like institutional barriers holding back breakthroughs. Instead, the entire network acts like a living, breathing organism—fluid, adaptive, open.

8.1 The Golden Age of Biotech

Through "tokenizing everything," from preclinical data to late-stage IP, coupled with decentralized governance, BIO exposes industry's greatest friction points. Suddenly, drug development feels more like science fiction than a drawn-out marathon.

8.2 Inclusive Community, Global Impact

This revolution isn't confined to the lab. Everyday investors—those with loved ones suffering from rare diseases—can stake tokens to support new research and witness transparent progress along the way. Collaboration is no longer a buzzword but an on-chain reality, propelling the formation of multinational research teams.

8.3 Reversing the Eroom Law

With friction removed, communities from any region can access global funding, and we might finally see the cost/time curve of drug development bend downward rather than upward—achieving the promised exponential scientific progress.

9. Grassroots Evolution of Biotech Financing

Andrew Lo's mega-fund theory points us to a crucial path: large, diversified portfolios can tame biotech's high risk and attract greater capital. However, top-down structures and institutional inertia still hinder the realization of certain innovations. In contrast, the BIO protocol disrupts this playbook:

· Community-Driven: Anyone with a stake—patients, scientists, or curious funders—can participate in governance, propose new BioDAOs, and collectively shape research directions.

· Tokenized IP: Data and IP become fluid, paving the way for new funding and collaboration models.

· Real-Time Liquidity: Breaking free from decadelong capital lockups, capital can swiftly flow into groundbreaking innovations.

· AI-Driven Risk Management: On-chain analytics continuously track performance, synergy effects, and correlations, allowing capital to flow efficiently across multiple BioDAOs.

By stacking decentralized scientific solutions (via BioDAOs) coordinated at the top layer of BIO (launchpad, funding, liquidity, meta-governance), the most daunting challenges in the science and pharmaceutical industries can be addressed in a community-driven, transparent, and continuously flowing environment.

Placing families, patients, and scientists at the heart of decision-making, BIO aims to 「boil the ocean」, tackling the dilemma of early-stage innovation. No longer shall half of the world's great ideas perish in the 「valley of death.」 Instead, we are witnessing the dawn of a science era unshackled from old gatekeepers and friction-filled pipelines.

So the next time your family faces a rare disease, the deciding factor will no longer be a boardroom's analysis of market size. It will be a global network—scientists, patients, and ordinary believers—collaborating, funding, and accelerating those therapies that truly matter. In short, we are back in a sci-fi world, where humanity unites to turn the impossible into the inevitable.

You may also like

SpaceX vs Tesla vs xAI: Which Elon Musk Trade Has the Biggest Upside in 2026?

OpenAI Reveals It Has Confidentially Submitted an S-1 to the SEC, Keeping the Door Open for a Future IPO

On June 9, according to an OpenAI announcement, the company recently confidentially submitted a draft S-1 registration statement to the U.S. Securities and Exchange Commission (SEC), beginning the preliminary compliance process for a potential initial public offering. OpenAI said it chose to disclose this proactively because it expected the news might leak; however, the company has not yet set a specific listing timeline, and related arrangements may still take some time.

Latest research from 13 top universities including Cornell University: The current state, challenges, and misconceptions of the fusion of Crypto and AI

Deconstructing Anthropic: The Best AI Company, Possibly Also a Type of Organizational Invention

Apollo and Blackstone Reportedly Back $35 Billion Anthropic Chip Financing as Deal Details Remain Unclear

On June 9, according to currently available news alerts, Apollo and Blackstone Group participated in a $35 billion financing for an Anthropic “chip project.” Based on the original wording of the report, the funding has already been raised, but public information remains limited. The financing structure, use of proceeds, project entity, and whether Apollo and Blackstone participated through equity, debt, or project financing have not yet been disclosed.

Humanity Protocol Security Incident Escalates: More Than $31 Million Stolen From Related Addresses as Attacker Continues Selling H for ETH

On June 9, according to monitoring by Onchain Lens, more than $31 million has been stolen from addresses linked to Humanity Protocol, and the attack is still ongoing, with the hacker continuously swapping H tokens for ETH. Project founder Terence Kwok later confirmed the security incident on X, saying the issue involved a private key leak.

Bloomberg: As Bitcoin Weakens, Stablecoins and RWA Continue to Drive Expansion in Crypto Businesses

In June, Bloomberg reported that despite Bitcoin falling below $60,000 last week, wiping out about $235 billion in market value within seven days, and dropping close to 50% from last year’s peak, some core businesses in the crypto industry are still expanding, mainly in stablecoins, real-world asset tokenization (RWA), payments, and infrastructure. The report also noted that overall altcoin activity has contracted significantly: altcoin market capitalization has fallen from a peak of about $431 billion in November 2021 to around $170 billion, and among the tens of millions of tokens issued in recent years, fewer than 1,700 still maintain meaningful trading activity.

Galaxy Deep Research Report: How Hyperliquid's HIP-4 Upgrade Changes the Landscape of Prediction Markets?

Binance Research: RWA Market Expected to Expand Nearly 6x from Early 2025, with Public Equities and Onchain Payments Heating Up Together

In June, Binance Research said in its monthly market report that the real-world asset (RWA) market is expected to grow by about 589% from the beginning of 2025. Bond- and money market fund-related RWA expanded by about $6.5 billion, up 83% year over year, while publicly traded equity RWAs grew by about 422%. The report also noted that monthly crypto debit card transaction volume exceeded $747 million in May, up 48.6% year to date.

Japan to Assess a Framework for Yen Stablecoins and Crypto ETFs as Asia’s Compliant Payments Narrative Heats Up

Recently, according to the original report, Japan is considering the launch of yen stablecoins and cryptocurrency ETFs. Public information remains limited at this stage, and there is still no complete policy text, regulatory draft, or clear implementation timeline, so this is better characterized as a “policy discussion” rather than formal implementation. The original wording also noted that advancing stablecoin regulation in Asia is driving XRP usage and supporting growth in the XRPL ecosystem. However, based on currently available public information, there is not enough evidence to directly establish a clear causal relationship between this round of discussion in Japan and XRP or XRPL.

ZachXBT: Humanity private key leak and abnormal surge in H token should be viewed separately

On June 9, according to related disclosures, on-chain investigator ZachXBT posted an update on Humanity’s roughly $31 million security incident, saying that after further analyzing fund flows, he currently tends to believe the project team was not involved in an “inside job” or a self-staged attack. According to him, the official explanation about the private key leak was broadly accurate, but before the token unlock, the price of H had been artificially pushed higher, and the hacker later took advantage of that market environment; therefore, the private key leak and the earlier abnormal price pumping should be regarded as two separate and independent events. This reframing has shifted the market’s understanding of the nature of the incident. Earlier discussion around Humanity had focused on whether the team directly participated in the attack or used the security incident to cover up internal operations. ZachXBT’s latest remarks shift the focus from “whether it was self-theft” to “whether there were pre-unlock market structure issues.” He also questioned whether the team may have.

Morning Report | OpenAI has submitted an S-1 registration statement draft to the U.S. SEC; Morpho completes $175 million financing

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

SpaceX vs Tesla vs xAI: Which Elon Musk Trade Has the Biggest Upside in 2026?

OpenAI Reveals It Has Confidentially Submitted an S-1 to the SEC, Keeping the Door Open for a Future IPO

On June 9, according to an OpenAI announcement, the company recently confidentially submitted a draft S-1 registration statement to the U.S. Securities and Exchange Commission (SEC), beginning the preliminary compliance process for a potential initial public offering. OpenAI said it chose to disclose this proactively because it expected the news might leak; however, the company has not yet set a specific listing timeline, and related arrangements may still take some time.

Latest research from 13 top universities including Cornell University: The current state, challenges, and misconceptions of the fusion of Crypto and AI

Deconstructing Anthropic: The Best AI Company, Possibly Also a Type of Organizational Invention

Apollo and Blackstone Reportedly Back $35 Billion Anthropic Chip Financing as Deal Details Remain Unclear

On June 9, according to currently available news alerts, Apollo and Blackstone Group participated in a $35 billion financing for an Anthropic “chip project.” Based on the original wording of the report, the funding has already been raised, but public information remains limited. The financing structure, use of proceeds, project entity, and whether Apollo and Blackstone participated through equity, debt, or project financing have not yet been disclosed.

Humanity Protocol Security Incident Escalates: More Than $31 Million Stolen From Related Addresses as Attacker Continues Selling H for ETH

On June 9, according to monitoring by Onchain Lens, more than $31 million has been stolen from addresses linked to Humanity Protocol, and the attack is still ongoing, with the hacker continuously swapping H tokens for ETH. Project founder Terence Kwok later confirmed the security incident on X, saying the issue involved a private key leak.